Real Estate

3/6/2026

February 2026 Market Snapshots

- Overall inventory has increased modestly to start the year, while transaction and dollar volume are running a bit slower than during the first two months of 2025. With relatively few closings so far in 2026, it is still too early to draw meaningful conclusions about pricing trends.

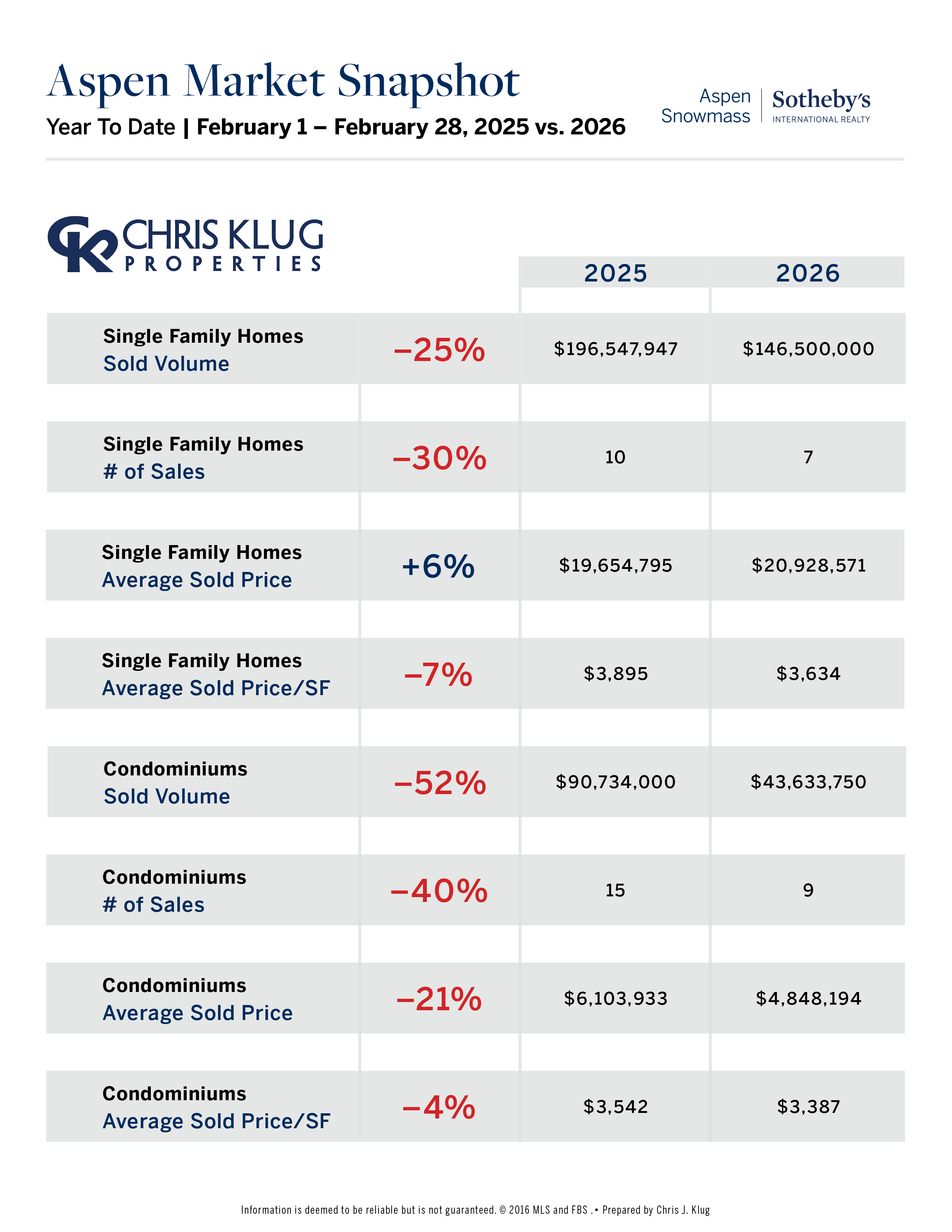

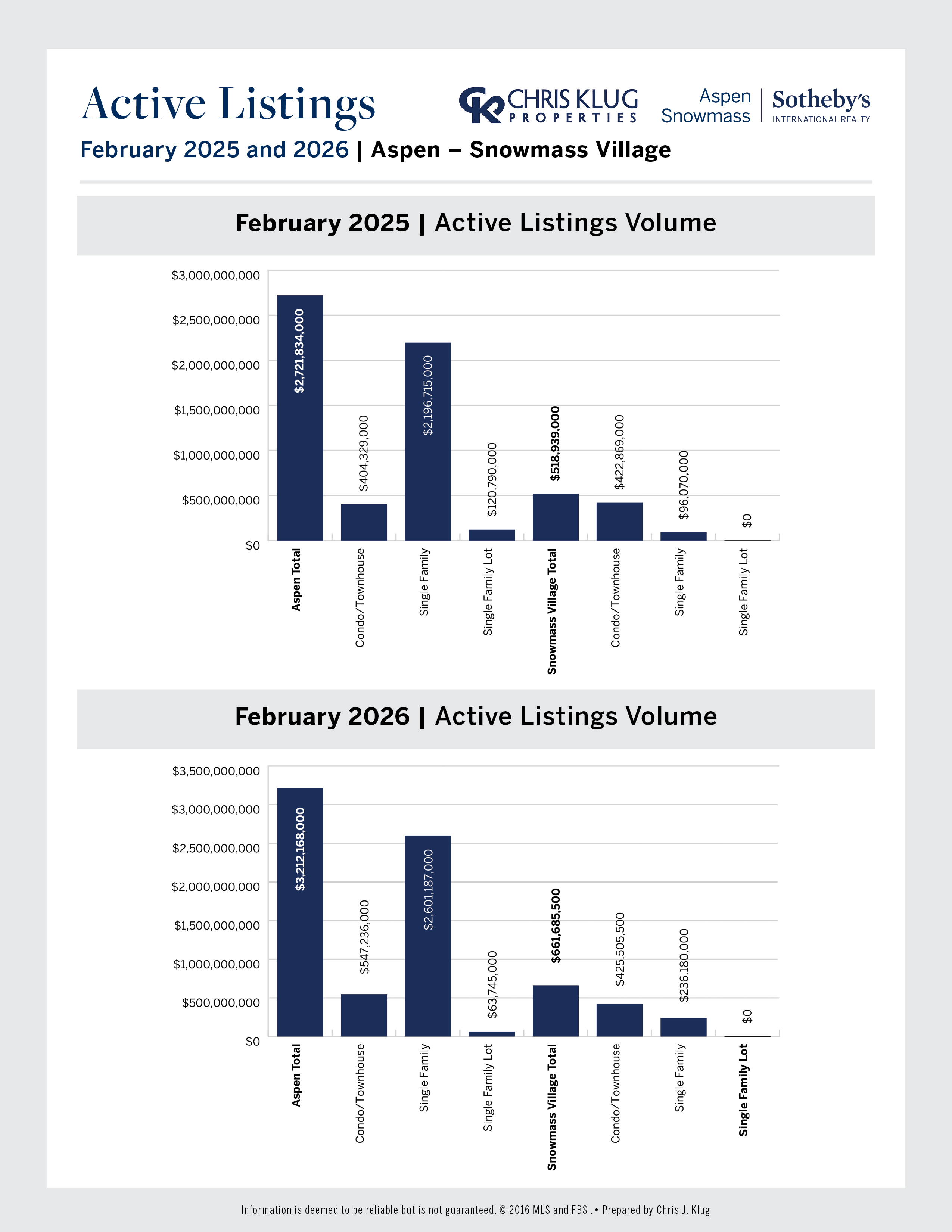

- In Aspen’s single-family market, sold volume and transactions are slightly lower than last February, although pricing remains relatively consistent with an average sold price of approximately $20.9 million. With only a handful of transactions year-to-date, however, pricing metrics should be viewed cautiously.

- Aspen’s condo market has seen a slower start to the year, with both dollar volume and transactions running at roughly half the pace of the first two months of 2025, and pricing down modestly.

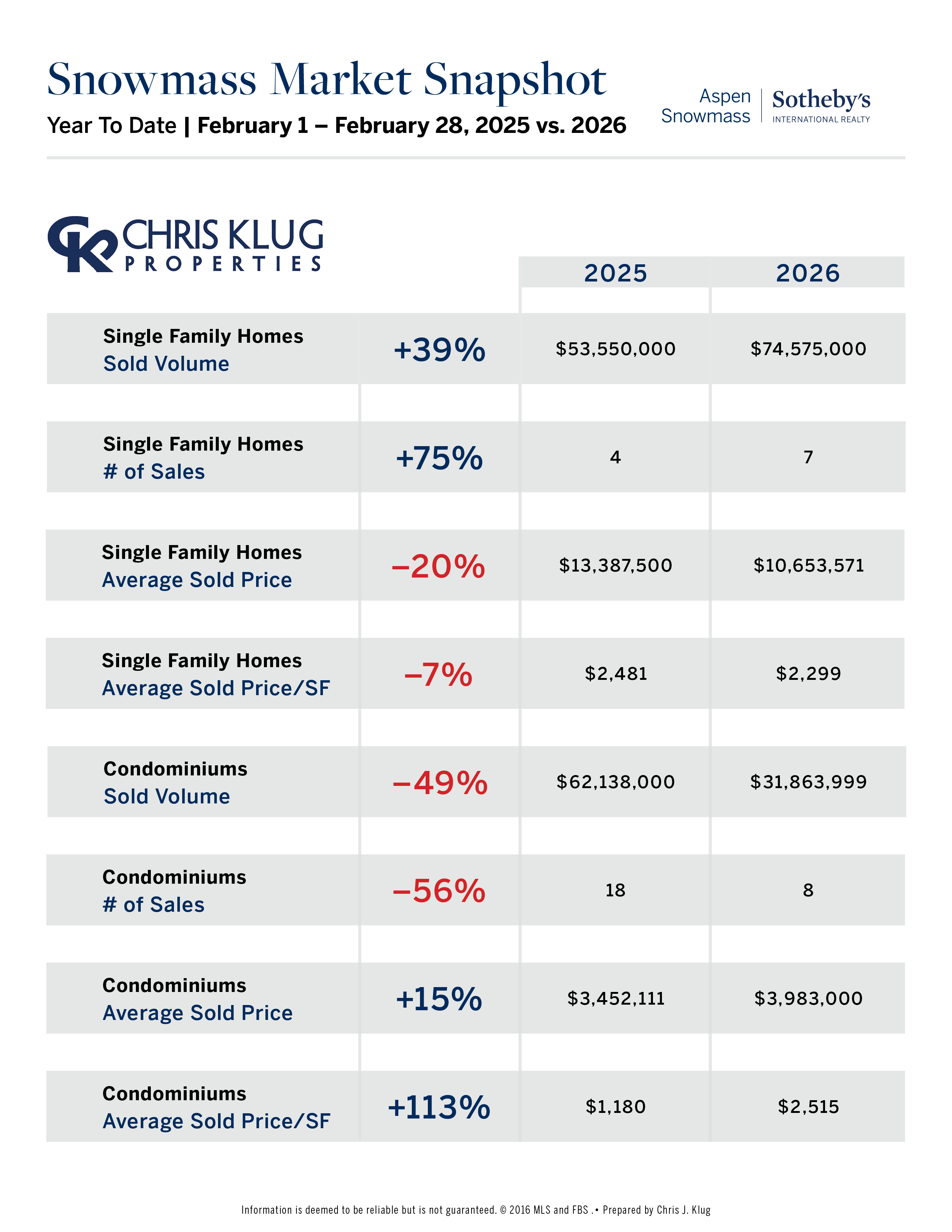

- Snowmass Village has been more active on the single-family side, where dollar volume is up nearly 40%, and transactions have increased about 75% year over year, although average pricing is slightly below last February.

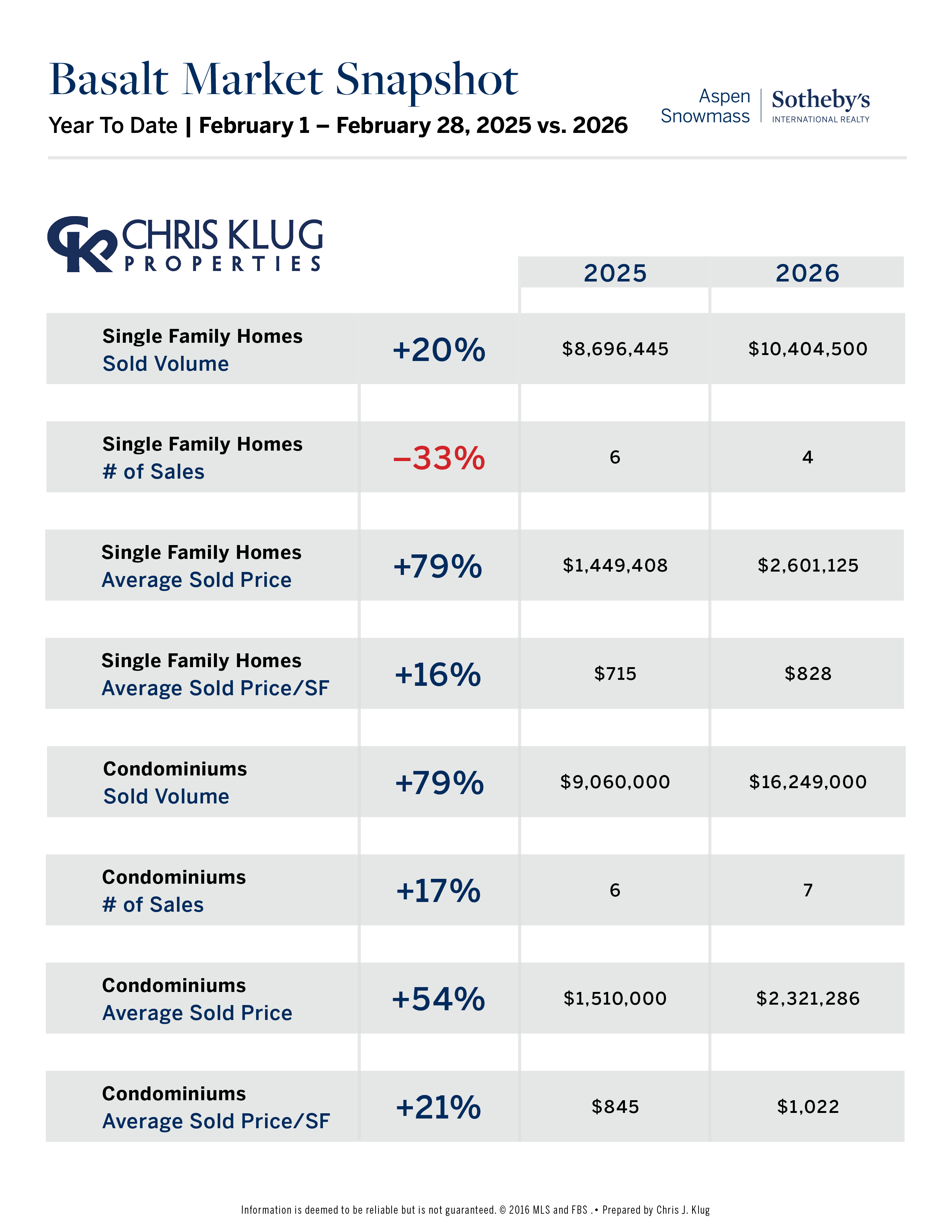

- In Basalt, activity has picked up with higher dollar volume and more transactions, and pricing is significantly higher compared to the same period a year ago.

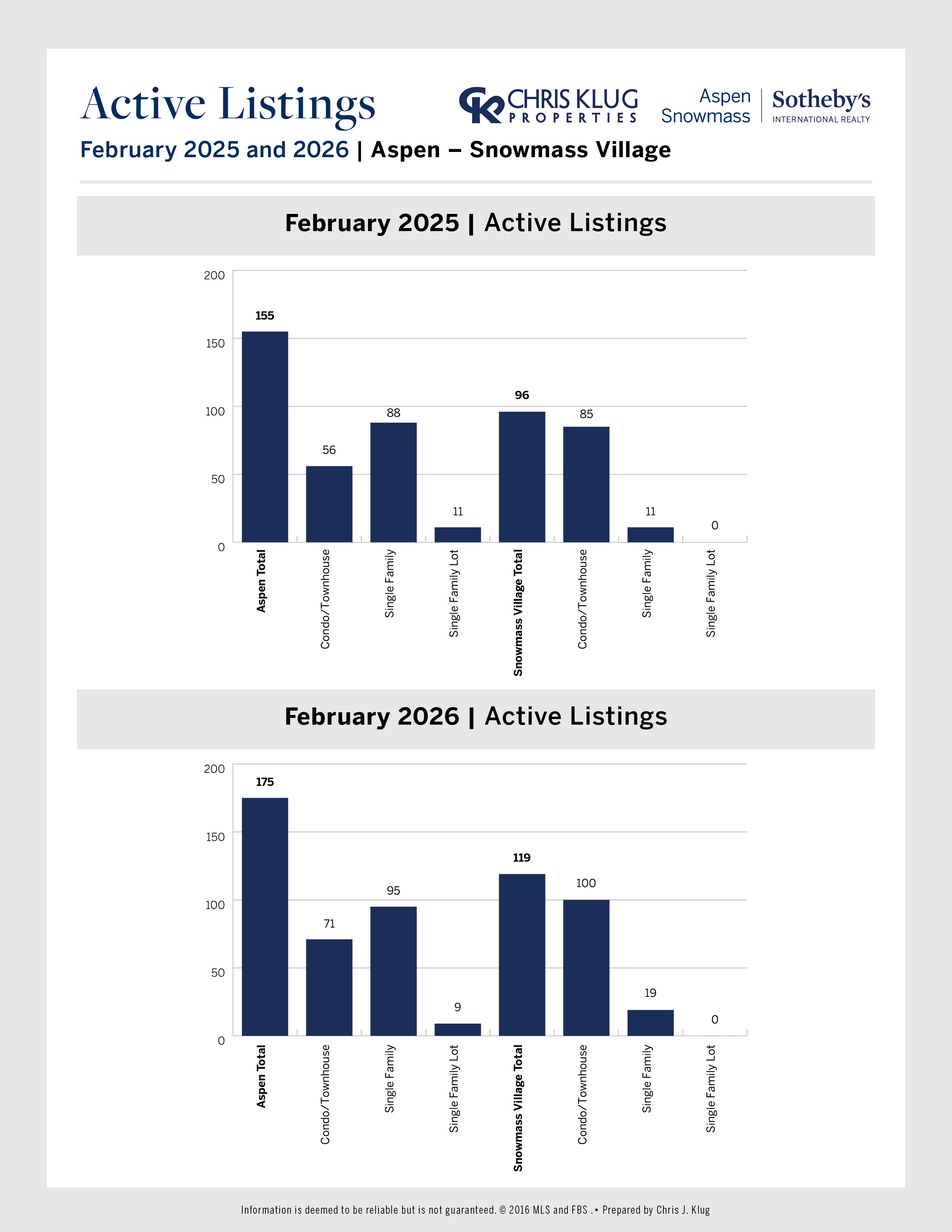

- Inventory across the Roaring Fork Valley remains historically tight but has improved slightly. From Aspen to Basalt, the active inventory of all free-market, whole-ownership property types increased from 366 properties a year ago to 412 as of February 28, 2026, representing a 12.5% increase.

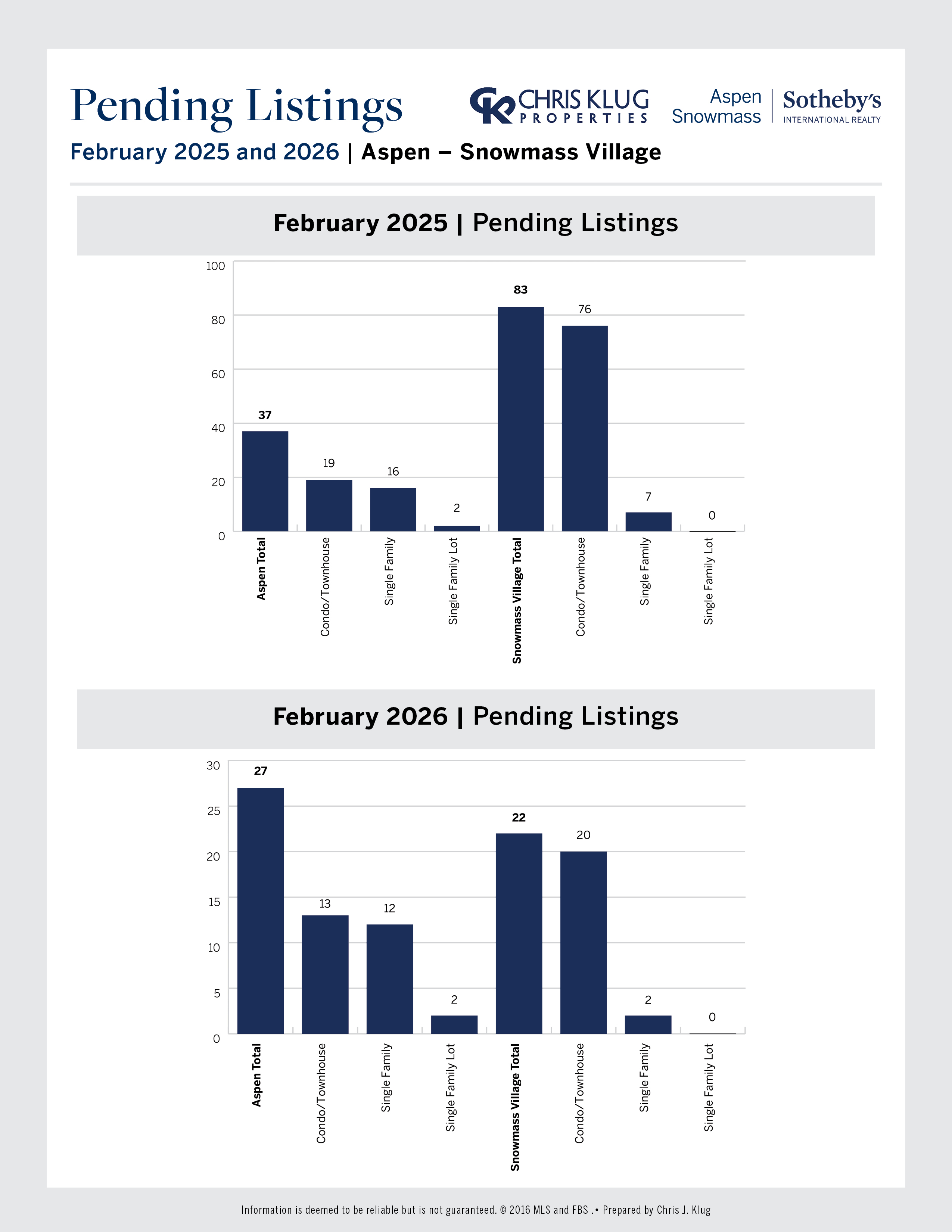

- In Aspen, overall inventory is up nearly 13%, with single-family homes increasing about 8%, condos up nearly 27%, and vacant land down roughly 18%.

- Snowmass Village inventory has increased more meaningfully, rising nearly 24% overall. Single-family inventory climbed 72%, although that increase represents a move from just 11 homes to 19 homes, which remains far below the 70 active listings that existed at the end of February 2020 before the pandemic. Condo inventory in Snowmass Village increased from 85 units last year to 100 today, a 17.6% gain, while vacant land inventory remains essentially nonexistent, with no available lots both last year and today.

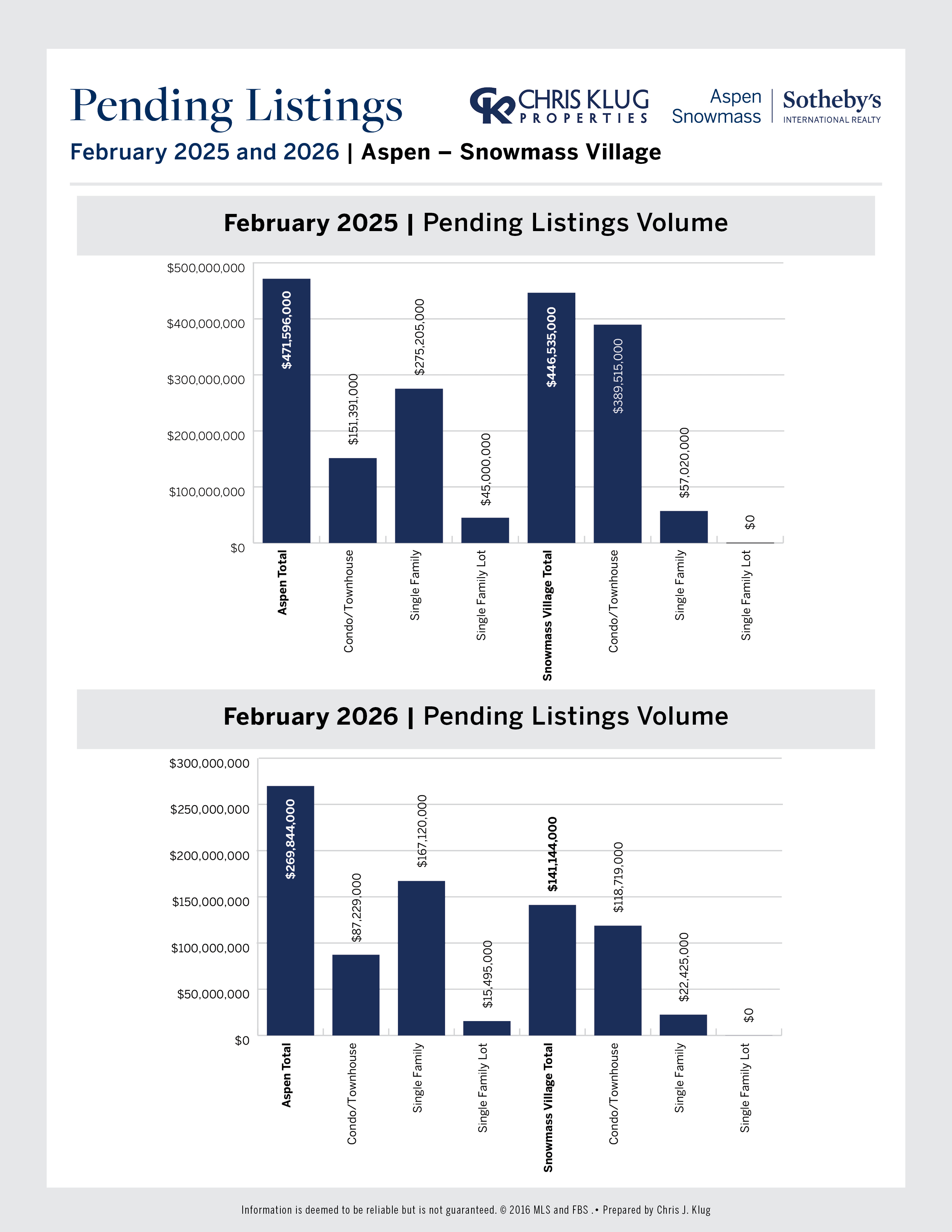

- Pending activity is currently running behind last year’s pace. At this point in 2025, there were 173 pending sales totaling just over $1 billion, compared to 78 pending transactions today totaling slightly more than $500 million, representing a 54% decline in pending transactions and roughly a 50% decline in pending dollar volume.

- It has been an unusual winter so far, but the prime weeks of spring break and the heart of the winter selling season are still ahead of us. There are plenty of productive conversations and showings happening across the market, and with fresh snow this morning, I remain optimistic about the remainder of the winter selling season.

- The ultra-luxury segment has been slightly quieter to start the year. $10 million-plus home sales in Aspen Snowmass declined 23%, from 13 a year ago to 10 so far in 2026, while $20 million-plus sales fell from 6 to 4, a 33% decrease. The highest sale year-to-date was a $42 million closing on McLain Flats, which I was proud to represent.